With a projected decline in farm equipment sales along with lower commodity prices, precision farming dealers aren’t immune to the effects these trends will have on sales of technology products. At the start of 2014, some dealers forecast hardware sales to remain flat or decrease, underlining the importance of developing alternative, sustainable revenue sources.

As one precision manager from Illinois notes, “Selling products will only take you so far in today’s precision market. You’d better be diversifying your business if you plan to stay in business.”

While hardware still bolsters the bottom line for many precision dealers, the 2014 Precision Farming Dealer benchmark study reveals a movement during the last year toward expanded service offerings, to include data management.

With nearly 90 respondents, the 2014 study builds on the foundation established last year, for an annual analysis of the performance trends and service objectives of precision farming dealers in North America. This year’s results provide some stark comparisons to the 2013 report, in terms of how dealers are shifting their precision business priorities, training personnel and assessing revenue targets for the coming years.

Independent Approach

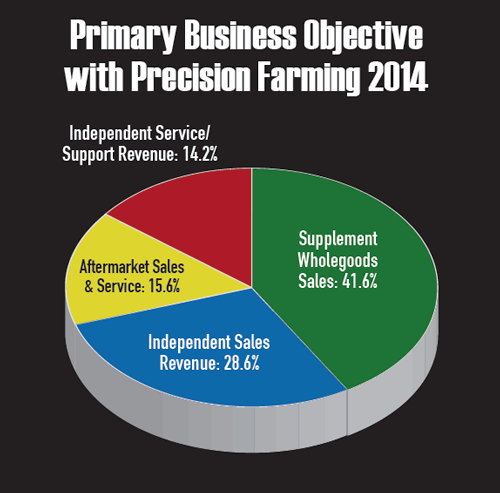

Developing precision farming as a sustainable source of revenue is an ongoing objective for many dealerships. One indicator that dealers are progressing in making precision a standalone business, rather than a supplemental source of income, is an increase in those who identified their primary objective with precision as being an independent money maker.

Based on responses from 27 states and Canada, 28.6% of dealers say their main goal with precision farming is to have it be an independent source of sales revenue, compared to 18.5% last year. The percentage of dealers who identify sales of precision service and support as their primary objective nearly doubled, from 7.7% in 2013, to 14.2% this year.

On the flip side, there was a substantial drop in dealers who identified their primary goal with precision business to supplement wholegoods’ sales, from 55.4% in 2013 to 41.6% this year. There was also a small dip in dealers whose main precision goal is aftermarket sales and service, from 18.4% last year to 15.6% in 2014. This isn’t surprising with more precision hardware coming factory installed on new OEM equipment.

However, dealers report a higher percentage of aftermarket precision product sales year-over-year, from 37.4% in 2013 to 52.1% this year. The percentage of precision products sold factory equipped on wholegoods dropped from 53.8% in 2013 to 40.5% this year.

These figures would seem to contradict what many dealers view as a shrinking precision aftermarket, but some may be capitalizing on adding precision technology to used farm equipment on trade-ins. It will be interesting to see if next year’s study reveals similar results.

One independent precision dealer in Iowa says, “We are losing more market share every year to OEM factory equipment. We are trying to find new sources of annually recurring revenue such as data management services, but it has been a tough sell to growers.”

If dealers continue moving toward independence with their precision business, success will likely depend on launching or broadening service platforms and relying less on hardware sales for the majority of revenue.

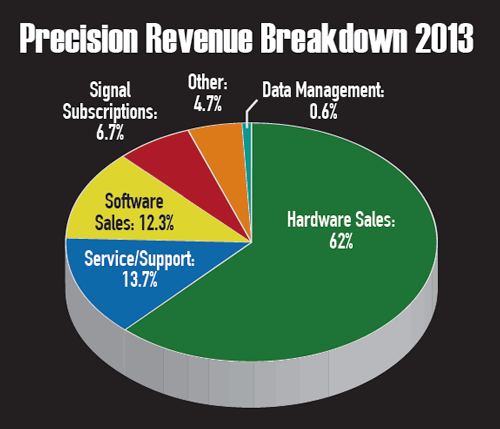

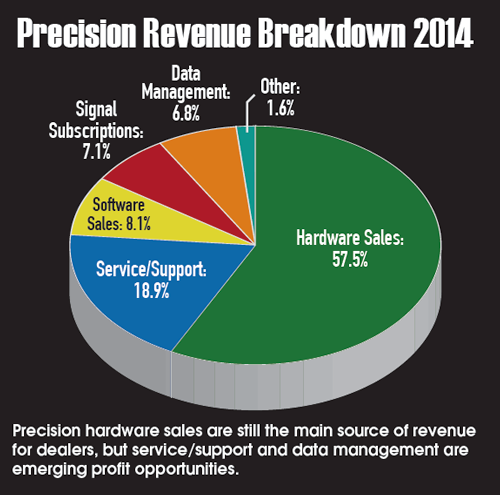

Despite a dip in the percentage of dealers whose main goal is selling precision products to supplement wholegoods, hardware sales remain the backbone of the precision business. Respondents say 57.5% of their precision revenue comes from selling hardware, down slightly from 62% in 2013.

The most significant revenue growth came in the areas of service/support sales, from 13.7% in 2013 to 18.9% this year, and data management, from less than 1% last year to 6.8% in 2014.

Although still small percentages compared to hardware, precision service and data management are emerging revenue opportunities dealers will likely continue to incorporate. However, unlike hardware, these areas are still relatively undeveloped in terms of a proven model that guarantees a financial return for the dealership.

As one Midwest dealer told us, “There’s no industry template for what to charge customers or what services to include. It’s kind of up to us to decide what’s going to be most successful at our dealership, try it and adapt it.”

Other revenue sources saw less substantial change, year-to-year, with software sales dropping from 12.3% in 2013 to 8.1% this year, and signal subscriptions increasing from 6.7% last year to 7.1% in 2014.

Expanding Staff & Service

As dealers continue to search for qualified hires, most maintain small precision staffs. This year’s study shows that 43.1% of dealers have 1-3 precision personnel throughout the company, compared to 58.2% in 2013. But while talent remains scarce, the percentage of dealers with 10-12 precision employees rose dramatically from 1.4% in 2013 to 11.6% this year.

It could be that dealership consolidation is contributing to larger precision departments as growing dealer groups absorb staff from acquisitions. The number of total stores dealers operate also increased year-over-year. This year, 24.4% of respondents reported operating 6-10 ag store locations, compared to 16.1% in 2013. Dealers with 11-25 stores also rose slightly (8.8% to 9.3%) as did those with 26 or more locations (1.5% to 3.5%).

Conversely, dealers with 1-2 locations dropped from 47.1% last year to 41.9% in 2014 as did the percentage of dealers with 3-5 locations (26.5% compared to 20.9%).

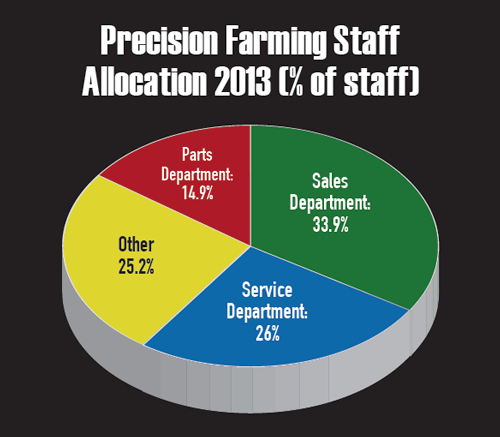

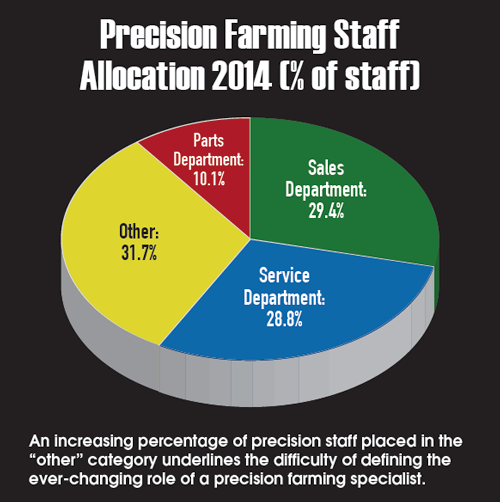

Consistent with last year, precision specialists continue to play diverse and unique roles within a dealership, with 31.7% classifying their precision staff as being outside of sales, service or parts. Placement in the “other” category is up from 25.2% last year, underlining the difficulty of defining the ever-changing role of a precision farming specialist. This may also indicate that dealers are establishing standalone departments and titles for precision business and personnel.

As several dealers note, keeping their specialists, let alone farm customers, up to date on the latest technology is an ongoing challenge. It often takes a combination of sales experience, tech-savvy and customer service skills to succeed as a precision specialist.

Salespeople account for the second largest portion of dealers’ precision staff, with 29.4%, down from 33.9% last year. Another 28.8% of precision staff are part of the service department, compared to 26% in 2013, and 10.1% are within the parts department, down from 14.9% last year.

Perhaps the diversity of roles precision specialists play at dealerships is providing flexibility to expand service offerings. Talking with dealers during the last year, many have adopted some form of precision support package, often with a suite of services available to customers.

Last year, only 29.8% of dealers said they offered a precision service package, compared to half this year (50.7%). This jump underscores the importance dealers are placing on recouping money for their service time.

The vast majority continue to charge an hourly rate for service (88.4% compared to 83.6% in 2013) and fewer are utilizing annual contracts (11.6% compared to 16.4% in 2013). But tracking billed service hours remains a challenge.

Asked to provide the number of annual service hours billed, dealer responses ranged from as few as 10 hours to as many as 8,000. More vague answers included “very few,” “unknown” and “not enough,” which were on par with replies in the 2013 study. The number of chargeable service hours dealers log can depend on the time of year, number of customers and availability of specialists.

One Canadian dealer notes that his biggest challenge is convincing not only customers, but dealership management, that the support they’ve traditionally given away as a “freemium” is worth the price of a service package.

“Providing excellent service and going the extra mile for these customers helps prove this value,” he says. “But another huge challenge is trying to show corporate management the true worth of providing customers with these services and how that service can influence future purchasing decisions.”

In this study, we ask dealers to identify from a list of 10 service offerings, which ones they offer, and for all but one — remote service, which was added this year — the percentages increased over 2013. The biggest jump was in data management, with the percentage nearly doubling year-to-year. Only 32.2% of dealers offered data management service in 2013, compared to 63.4% this year.

As some dealers move toward being a “one-stop shop” for data management service, it was no surprise that related services also saw significant increases, including GPS/RTK signal subscriptions, (61% to 81.7%), yield monitor calibration, (71.2% to 90.1%), soil sampling (8.5% to 18.3%) and seed and fertilizer recommendations (10.2% to 19.7%).

Nearly every dealership (97.2%) continues to offer precision equipment installation for customers, compared to 96.6% in 2013, and the vast majority also do pre-season setups/training (83.1%, up 5% from 2013) and in-season technology support (93%, up 7% from 2013).

The overall increase in service offerings reinforces the significance dealers are placing on these areas to distinguish themselves from the competition and create new revenue opportunities.

Big Data Gains Ground

Last year, data management was still largely a buzzword for many precision dealers, but it was clearly a focus in 2014. More than half (54.1%) of dealers say they offer data management services in conjunction with sales of precision products, compared to 31.1% in 2013.

Only 18.9% say they plan to add data management service in the future, compared to 31.1% last year, suggesting that a fair number of dealers may have already added the offering to their precision arsenal.

But this area has also become increasingly complex with a variety of companies offering new platforms for collection and analysis of farm information, along with questions about data security and ownership. A precision farming manager in Indiana says his biggest challenge is getting farm customers to use data to their advantage.

“My number one goal is to make it easier for customers to collect data so they’ll be more apt to try to use the information,” he says. “It’s been too difficult for farmers to deal with transferring the data and if we can make that easier, then agronomists and consultants can do their job and everyone wins.”

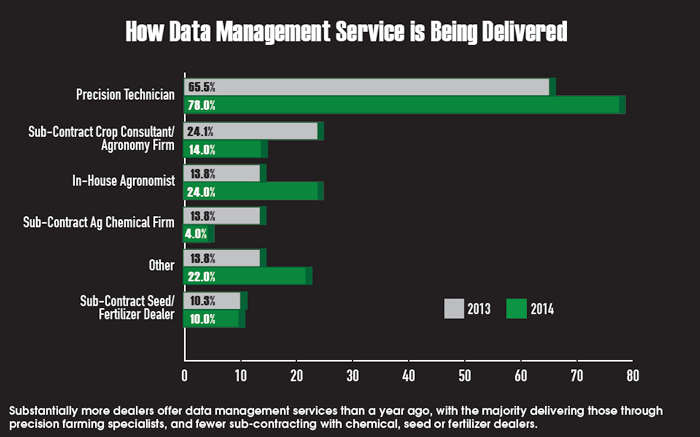

Delivery of data management service is also an evolving process for dealers. The most popular option is through precision farming specialists, with 78% of dealers preferring this method, up from 65.5% in 2013. Many dealers have begun to offer in-house yield mapping or data transfer service to farm customers as an entry point into data management.

Others continued a more aggressive path to delivery of these services with 24% of dealers using in-house agronomists, up from 13.8% doing so in 2013. Sub-contracting with crop consultants, local chemical firms or seed and fertilizer dealers were less popular options, with each seeing declines year-over-year. However, some precision industry professionals suggest that partnerships — which may differ from sub-contracting — could be the way many dealers ultimately establish themselves with data management service.

It will be interesting to see whether dealers continue to deliver and expand data management service through their own specialists, embrace outside options or find success somewhere in between.

The Next 5 Years

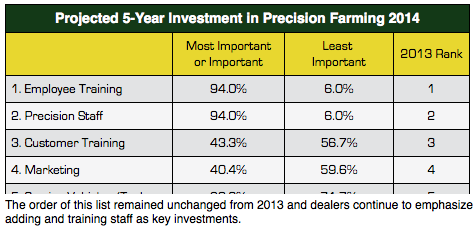

As dealers identify future precision growth opportunities, the main targets are adding and training employees. These two areas tied for first, with 94% of dealers projecting their most substantial investment in precision will be in new hires and employee training during the next 5 years. Last year, employee training ranked first (96.3%) and additional precision staff ranked second (91.2%).

Not surprisingly, specialist training and adding staff also ranked first (92.7%) and third (85.2%), respectively, on the list of greatest needs to grow dealers’ precision business during the next 5 years. Last year, staff additions was first (88.9%) and technician training ranked third (87%).

While dealers place a priority on expanding and training staff, it’s also one of their biggest challenges. Several cited a “lack of personnel,” “finding a keeper” and “hiring the right people” as their biggest anticipated problem during the next year.

Still, with precision specialists increasingly adding responsibilities, dealers are providing a higher percentage of in-house training compared to 2013. Last year, about a quarter (24.1%) of dealers said 51-75% of specialist training was done in- house, compared to 37.1% in 2014. The percentage of dealers doing 76-100% of training in-house nearly doubled, from 6.9% in 2013 to 11.4% this year.

Part of this increase could be attributed to more dealers cross-training equipment mechanics and parts staff on precision farming service. One Illinois dealer says they’ve set training and education goals for farm equipment sales and service personnel to integrate them into the precision side of the business, and reduce the burden on specialists being the only technology touch point with customers.

Although more dealers are offering a higher percentage of in-house training, only 22.5% say this is where specialists receive the majority of their professional development. Dealers turn to manufacturers for 69% of specialist training, while 7% comes from online offerings and 1.4% is from independent sources.

It will be interesting to see if online opportunities increase, as a matter of convenience and also as more dealers begin to produce and publish in-house tutorials on YouTube or dealership websites.

Customer training also remains an ongoing focal point for dealers. This year, customer training ranked second (89.7%) on the list of greatest needs to grow precision farming operations, consistent with last year’s ranking (87%).

A new category this year asked dealers to share the types of training opportunities offered to customers and 94% offer pre-season clinics. Interestingly, precision ag field days ranked second (54.6%), and more dealers seem to be leveraging these events as education, customer service and sales opportunities.

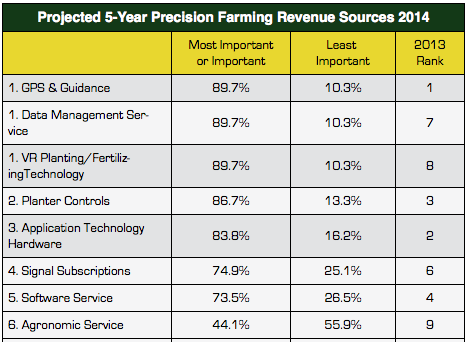

But the end result of dealers’ investment in staff or customers is to increase revenue. Last year, dealers identified GPS and guidance systems (91%), along with application technology (85.8%) as the top two areas for revenue growth during the next 5 years.

Both areas remained high priorities for dealers, but GPS and guidance tied for the top spot with data management service and variable-rate planting/fertilizing technology, with 89.7% of dealers projecting these areas as most important or important to growing revenue.

Last year, data management ranked seventh on the list (67.9%) and variable-rate planting/fertilizing technology (modified from variable-rate fertilizing in 2013) ranked eighth (60.8%). These dramatic jumps reinforce dealers’ evolution from hardware-driven businesses to more diversified service-based models.

Planter controls ranked second (86.7%), up one spot from 2013 (76.9%), and dealers say they see rising interest from farmers in planting technology such as row clutches, given the tangible return on investment, especially heading into a market slowdown.

One North Dakota dealer says, “In a market downturn, we wonder if precision farming technology will be the first off of a customer’s purchase list in order to make ends meet. We want to show the growers that it should be the last off the list.”

New to the list this year was unmanned aerial vehicles, which ranked last on the list (27.9%). While this wasn’t surprising given the unknowns surrounding application and proven value of the technology in agriculture, it will be interesting to see if this is an area of emphasis for dealers in the future.

![[Technology Corner] Using Sensors to Measure Impact of ‘Soil Health Management’ Systems](https://www.precisionfarmingdealer.com/ext/resources/2026/07/24/Using-Sensors-to-Measure-Impact-of-Soil-Health-Management-Systems.webp?height=290&t=1784914811&width=400)